Attention Downsizing Baby Boomers – Sell Your House, Protect All Your Equity, and Pay NO Capital Gains Taxes with this Simple Strategy Using Tools Congress Gave Us

Many of my parent’s friends who have fortunately accumulated significant equity in their homes over the last several decades are faced with a dilemma of downsizing into a smaller home because they can no longer conveniently or adequately take care of their properties. Importantly, many of them desire a simpler-smaller property, usually all single-level, accessible and easy to maintain. The problem exists because if they sell their home with substantial equity they face significant capital gains exposure even with the IRC Section 121 exclusion in place.

For example, a married couple may exclude from capital gains tax $500,000 (Sec. 121) if they have resided in their primary residence two (2) out of the last five (5) years. So, if a couple has accumulated $2,000,000 in equity in their home (after improvements and original purchase price) they would still have a $1,500,000 capital gain. In California, with all of the taxes included, the capital gains rate is approximately 33% (highest in U.S.). Thus, this couple would have to pay approximately $495,000 in capital gains taxes in the next tax year after their sale. So how do we get around this challenge?

Congress Is On Your Side Sometimes – Believe It or Not

With the Congressional enactment of the American Jobs Creation Act of 2004 and the Housing and Economic Recovery Act of 2008, and Department of the Treasury Revenue Procedure 2008-16 the government has made it easier for homeowners to keep more of their equity – and even not pay any capital gains taxes, ever – if they don’t want to.

Internal Revenue Code Section 121 (The “121 Exclusion”)

This code section says that if a property is your primary residence and you (or you and your spouse) have lived in it for two (2) out of the last five (5) years you can sell the property and exclude from taxes $250,000 if you are single, or $500,000 if you are married and file a joint tax return. This code does not apply to second homes, vacation homes, rental homes, or investment properties. Another wrinkle is that you can only exclude capital gains and not recaptured depreciation (but that is another article).

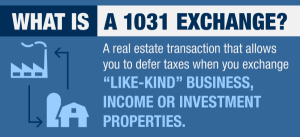

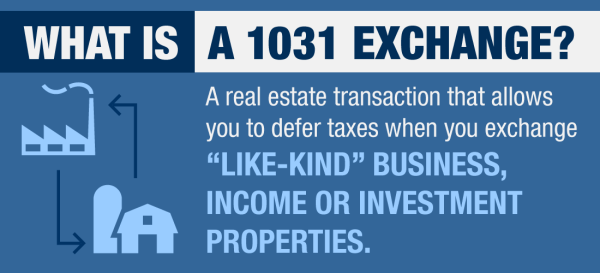

Internal Revenue Code Section 1031 (The “1031 Exchange”)

Internal Revenue Code Section 1031 (The “1031 Exchange”)

A 1031 exchange allows a person to sell a property (“relinquished property”) that was held as a rental or investment property and then exchange the proceeds from that sale into a new “like-kind” property (“replacement property”) also to be held as a rental or investment property. The benefit of using a 1031 exchange is that no matter what capital gains you may have accumulated in the “relinquished” property they are all transferred into the “replacement” property and no taxes are due or payable at that time. The taxes are deferred into the replacement property. The 1031 exchange does not apply to a primary residence, but you can convert your primary residence into a rental property and take advantage of all its benefits.

Combining IRC Section 121 and IRC Section 1031 Is Powerful

Over the 239 years or so that this country has existed there has never been one set of laws that allowed more American families to accumulate more wealth than Section 1031. Mind-boggling multi-generational wealth has been created by clever investors who never pay capital gains taxes on their real estate portfolios even though they keep selling and buying more and more and bigger and bigger buildings.

With careful and meticulous tax planning people can combine both IRC 121 and 1031 to legally avoid and/or defer all capital gains taxes on the sales of real property – while improving the assets by buying bigger and better buildings each time one is sold.

Three Different Methods of Converting Properties for this Strategy

There are three (3) distinct transactions which these two code sections will allow sellers/investors to take full advantage of the code.

- (1) Rental Property Converted to a Primary Residence (no prior 1031 exchange)

If you bought an investment/rental property and later wanted to convert it to a primary residence you will have to move into the property for a minimum of 2 years to qualify for IRC 121. There are some other restrictions but the main benefits of 121 + 1031 are still available to you.

- (2) Rental Property Converted to a Primary Residence (prior 1031 exchange)

This case is similar to 1 above. The difference is that the original purchase of the investment property was done with a 1031 exchange. The minimum time you will have to own this property is five years to qualify for IRC 121 exclusion and then you can 1031 exchange it again. You do not have to live it in for five years, but only two out of the last five years. There are some other restrictions but the main benefits of 121 + 1031 are still available to you in this fact pattern.

- (3) Primary Residence Converted to a Rental Property – The Golden Strategy

This is the golden strategy that applies to many people. The Internal Revenue Service drafted Revenue Procedure 2005-14 which allows you to move out of your primary residence and convert it into a rental property. Although there is no rule or statute it is common practice that a person should rent the converted property for a minimum of one year (I always say a year and a day with full intention of making it a rental). The year and a day rule of thumb cures the primary residence into a “rental/investment” property. Now you can sell the rental/investment property and take advantage of IRC 121 ($500,000 exclusion) and 1031 exchange the property into another, more profitable or desirable building – thus deferring any leftover capital gains exposure.

But Where Am I Going To Live?

When I talk to people about this strategy the first question they always ask is “[W]here am I going to live? The answer is “[A]nywhere you want to.” A person can take the proceeds of the rental income from their newly converted rental property and go and rent somewhere else for the 12 or so months why the property is “curing.” In fact, most of the time the rental/investment property will kick-out substantial rental income such that the owner can find suitable rentals and still have left over monies each month (more than likely their mortgage obligations on their primary residence is exhausted).

I tell my clients to look for something to rent on a golf course, a simple single-level condominium, or a beautiful unit in a high-rise building. There are so many different options all of which can be afforded by the budget from the rental income.

What Will I Buy with the 1031 Exchange Proceeds?

I have always counseled my clients to look for a commercial building or a mixed use building to exchange into. Well positioned commercial buildings will typically have tenants on triple-net leases where the tenant is paying more than 100% of the actual expenses of the building including property taxes, insurance, improvements, etc.

If you purchase a building with greater value than the proceeds from the relinquished property just make sure the amount of rental income will be enough to cover your expenses. A discussion about capitalization rates for commercial buildings was covered in a previous article I wrote right here http://bit.ly/VmlTeB.

A mixed use building with retail and residential components are attractive because the owner may decide to live in one of the residential units. You can also hire a professional property manager to manage your property for you to relieve you of any associated duties – and their fees are tax deductible.

The ultimate answer is it really doesn’t matter. There are so many opportunities that exist the possibilities are endless.

Step By Step Procedure Looks Like This

Step 1. Accumulated Equity Above $1,500,000

Step 2. Move out and convert primary residence to rental for a year and a day

Step 3. Find rental for you to live in with proceeds from renting your previous primary residence

Step 4. After 12 months or so sell the rental/investment “relinquished” property to take advantage of Sec. 121

Step 5. 1031 exchange the proceeds of the relinquished rental sale into a new building

Step 6. Identify “replacement” property within 45 days of the sale and close escrow within 180 days of sale of “relinquished” property

Step 7. Continue to rent at your discretion – or find a new rental – or move into the “replacement” property

Step 8. Enjoy the benefits of keeping your assets within your family and plan to keep the “replacement” property in the family succession

Now You Know How to Sell Your House, Keep All Your Equity for Your Family, and Pay NO Capital Gains Taxes

Now You Know How to Sell Your House, Keep All Your Equity for Your Family, and Pay NO Capital Gains Taxes

As I started this article I told you that many of my parent’s friends have accumulated significant equity in their homes over the last several decades and now they are looking to downsize but are faced with this problem. This problem exists for thousands of retiring baby boomers (especially here in the Bay Area). I have shown them, and now you, tools that the government has given us which affords us an opportunity to keep all of our assets without having to pay any capital gains taxes. This is not a complicated strategy, but it does require due diligence, patience, and a desire to accomplish your goals. Hiring a real estate professional to help you through this process is key. Please don’t hesitate to contact me with questions, inquiries or ideas. I’d love to hear from you about this topic.

Great information….I wonder how many agents will actually use it.

Thanks Again,

Robin